Ever wondered why bitcoin futures prices tend to be higher than normal market price? With the new OKCoin quarterly contract coming out, some discussion around how futures prices are determined is being had. A lot of traders get confused about why exactly Futures prices tend to be in a premium to the index/spot price that it settles at. Intuitively traders know that when it's bullish and people are buying a lot, then the premium will be higher, and conversely when things get bullish and people are selling hard, it can even enter a discount to the spot.

Some Finance 101 (or maybe 102) shows how you can calculate what the "fair value" of these contracts would be, given no arbitrage being possible. You can replicate the future value of a bitcoin in USD by borrowing USD and buying BTC. The price of the Forward then should not deviate far from this level or arbitageurs close it.

This material is inspired partially from Arthur at BitMEX's arbitrage trading YouTube presentation here.

The efficient pricing of Futures contracts theoretically in finance is then governed by this formula:

F = S * ( 1 + Rh * t ) / (1 + Rf * t)

Where F = the price.

S = spot price

Rh = home interest rate

Rf = foreign interest rate

t = days / 365

Just as an example, using Bitfinex swap markets as the baseline, at a spot rate right now of $410 , USD rate of 9% APY and BTC rate of 2% APY, and a quarterly maturity of 90 days. Home = USD, Foreign = BTC. Its not exact, but we will use as a simple rate for quarter on USD at 2.25% and 0.5% on BTC.

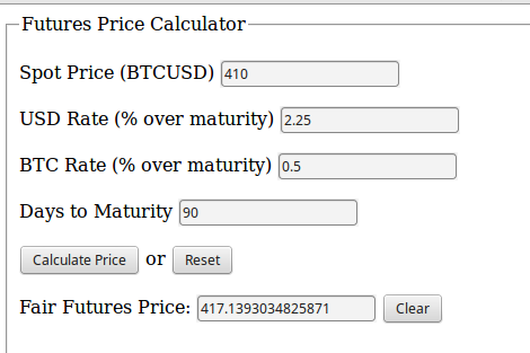

Here is a simple Bitcoin Futures Fair Price Calculator which you can plug these values into and you will get:

Some Finance 101 (or maybe 102) shows how you can calculate what the "fair value" of these contracts would be, given no arbitrage being possible. You can replicate the future value of a bitcoin in USD by borrowing USD and buying BTC. The price of the Forward then should not deviate far from this level or arbitageurs close it.

This material is inspired partially from Arthur at BitMEX's arbitrage trading YouTube presentation here.

The efficient pricing of Futures contracts theoretically in finance is then governed by this formula:

F = S * ( 1 + Rh * t ) / (1 + Rf * t)

Where F = the price.

S = spot price

Rh = home interest rate

Rf = foreign interest rate

t = days / 365

Just as an example, using Bitfinex swap markets as the baseline, at a spot rate right now of $410 , USD rate of 9% APY and BTC rate of 2% APY, and a quarterly maturity of 90 days. Home = USD, Foreign = BTC. Its not exact, but we will use as a simple rate for quarter on USD at 2.25% and 0.5% on BTC.

Here is a simple Bitcoin Futures Fair Price Calculator which you can plug these values into and you will get:

Using this metric, the expected premium then on the OKCoin quarterly expiring in 90 days will be about $8, and if spot is still around $410 its price will be a bit over $417.

Now this does not take into account the bullish and bearish sentiment that drags the fair price around. When things get really volatile then it will deviate greatly from this.

Looking over at CryptoFacilities you can see that this contract already exists and is somewhat efficiently priced:

Now this does not take into account the bullish and bearish sentiment that drags the fair price around. When things get really volatile then it will deviate greatly from this.

Looking over at CryptoFacilities you can see that this contract already exists and is somewhat efficiently priced:

It is a fair bit higher than the fair price calculation. But keep in mind that the rates we used from Bitfinex are not the only market rates. Volatility is also a major consideration, as well as sentiment. People have other rates they can get for borrowing USD lending out BTC. These are different for market participants in different risk profiles.

Play around with the calculator and see what the fair value is for the rates you can get. It is useful to keep in mind this price when volatility hits and there are deep discounts or steep premiums.

Play around with the calculator and see what the fair value is for the rates you can get. It is useful to keep in mind this price when volatility hits and there are deep discounts or steep premiums.

RSS Feed

RSS Feed