Bitcoin derivatives exchange BitMEX has made another strategic pivot recently by announcing they were going to stop issuing new futures contracts and instead focus on new swap products which pay (and deduct) interest from users who are short (or long). Perhaps most importantly: the contract never expires, so you are never forced out of your position because of any settlement.

They started by releasing the ETHBTC and have now swept their product offering of futures with this new swap product. There's a lot of confusion surrounding this new product, but it can be quite simple once you understand a few financial principles. Patiently read through this article if you would like to understand why there's a premium, and what the Bitfinex BTC and USD rates have to do with the price of futures and the behavior of the BitMEX XBTUSD swap.

They started by releasing the ETHBTC and have now swept their product offering of futures with this new swap product. There's a lot of confusion surrounding this new product, but it can be quite simple once you understand a few financial principles. Patiently read through this article if you would like to understand why there's a premium, and what the Bitfinex BTC and USD rates have to do with the price of futures and the behavior of the BitMEX XBTUSD swap.

What does the future value of BTCUSD represent?

In financial theory, it's quite simple how this is done. The future value of BTC/USD is merely the realisation of what a creditworthy individual can do by borrowing USD to invest in BTC. You can play with our Fair Price calculator here to see how different rates affect the theoretical equilibrium value of BTCUSD in the future.

In our post on Why Bitcoin Futures Tend to Trade at a Premium to Spot, we went briefly into the Covered Interest Parity and how this is a major indicator of the proper futures rate because it shows the arbitrage condition. Let's revisit this concept in a different light to understand the BitMEX swap product XBTUSD.

In practice there are frictions in the market. You can't fluidly go to Bitfinex and borrow BTC in order to sell it for USD, which you then use to lend out at a higher rate than you borrow BTC. This requires collateral, which defeats the purpose, and fees and other costs make this less easy too. However, in a well adjusted and efficient market, this is how the prices are governed, so try to keep an open mind and understand the theory behind it without getting too autistic about the practical details.

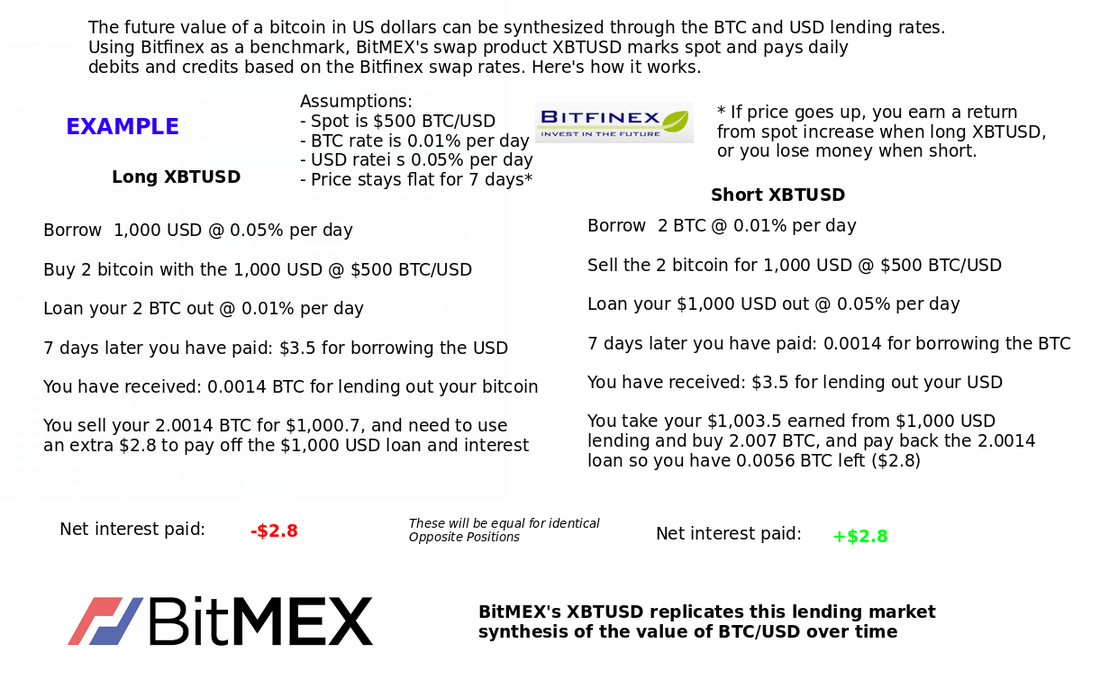

Just like in our infographic above, we make the same assumptions, BTC/USD = $500, USD borrow and lending rate is 0.05% per day at Bitfinex, and BTC rate is 0.01%. Let's say then that the futures price for a weekly contract settling in 7 days was the same price, $500. An arbitrageur sees this price and thinks, wait, can't I borrow BTC at 0.01% and just sell them for USD and lend out at 5x the rate at 0.05% and earn a return? He would earn each of those rates every day for 7 days, paying 0.07% in bitcoin and earning 0.35% in USD. In his mind, $500 is a bargain because he can actually really make:

1.0035/1.007 * 500 = $501.4

Just by earning the interest differential. This incentivizes him to then buy the $500 future because he can synthesize the value of bitcoin in 7 days in the financing market and sell at $501.4.

This market pressure through arbitrage leads eventually to the market price of the 7-day BTCUSD future to converge to this Covered Interest Parity price.

In our post on Why Bitcoin Futures Tend to Trade at a Premium to Spot, we went briefly into the Covered Interest Parity and how this is a major indicator of the proper futures rate because it shows the arbitrage condition. Let's revisit this concept in a different light to understand the BitMEX swap product XBTUSD.

In practice there are frictions in the market. You can't fluidly go to Bitfinex and borrow BTC in order to sell it for USD, which you then use to lend out at a higher rate than you borrow BTC. This requires collateral, which defeats the purpose, and fees and other costs make this less easy too. However, in a well adjusted and efficient market, this is how the prices are governed, so try to keep an open mind and understand the theory behind it without getting too autistic about the practical details.

Just like in our infographic above, we make the same assumptions, BTC/USD = $500, USD borrow and lending rate is 0.05% per day at Bitfinex, and BTC rate is 0.01%. Let's say then that the futures price for a weekly contract settling in 7 days was the same price, $500. An arbitrageur sees this price and thinks, wait, can't I borrow BTC at 0.01% and just sell them for USD and lend out at 5x the rate at 0.05% and earn a return? He would earn each of those rates every day for 7 days, paying 0.07% in bitcoin and earning 0.35% in USD. In his mind, $500 is a bargain because he can actually really make:

1.0035/1.007 * 500 = $501.4

Just by earning the interest differential. This incentivizes him to then buy the $500 future because he can synthesize the value of bitcoin in 7 days in the financing market and sell at $501.4.

This market pressure through arbitrage leads eventually to the market price of the 7-day BTCUSD future to converge to this Covered Interest Parity price.

Covered Interest Parity makes sense, so what does this mean for swaps?

The prior section was just a refresher on how the BTC and USD financing markets affect the price of futures contracts, which themselves represent the future value of Bitcoin in USD. Now, turning back to BitMEX's swap product, which is a "Perpetual Swap", what difference is there between buying XBTUSD and holding it for 7 days, and buying a BTCUSD futures contract expiring in 7 days? In theory, there is no difference, both are just different ways to arrive at the future value of Bitcoin in USD.

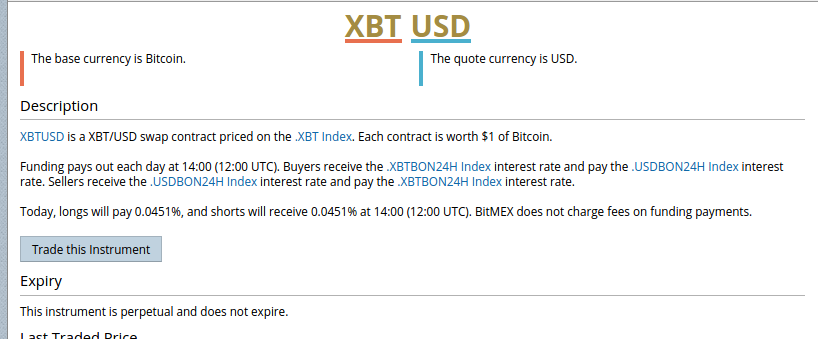

With this in mind, we look at the BitMEX XBT swap contract specifications:

With this in mind, we look at the BitMEX XBT swap contract specifications:

Remember that BitMEX is a pure-bitcoin site, so you are only depositing and trading with BTC as collateral. However, each contract on XBTUSD represents $1 in value. Just like their futures contracts, every contract has a customer as counterparty who is on the LONG and the SHORT side.

Each day at 12:00 UTC, the long holders of XBTUSD pay the USD lending rate, and receive the BTC rate. The short holders of XBTUSD receive the USD lending rate and pay the BTC rate. The example in our infographic is USD rate (0.05%) - BTC rate (0.01%) = net financing rate 0.04%.

You might be wondering: hey, why would anyone stay long if they know they are going to pay this stupid daily rate? Why not just sell it 1 hour before and avoid it? The answer is: it is more expensive to do this because you will pay a 0.075% fee to do a taker sell in order to get out. This means that nobody who is rational will be offering you the ability to get out and profit from missing the payment that a long holder has to have. Similarly for those who want to make a quick short interest payout, they can't simply short at a market price that will be above spot, allowing them to earn the interest without any cost.

The closer to this 12:00 UTC daily payment, the more the market discount will be to reflect this inability for long or short holders to arbitrage and get a free lunch from this.

Each day at 12:00 UTC, the long holders of XBTUSD pay the USD lending rate, and receive the BTC rate. The short holders of XBTUSD receive the USD lending rate and pay the BTC rate. The example in our infographic is USD rate (0.05%) - BTC rate (0.01%) = net financing rate 0.04%.

You might be wondering: hey, why would anyone stay long if they know they are going to pay this stupid daily rate? Why not just sell it 1 hour before and avoid it? The answer is: it is more expensive to do this because you will pay a 0.075% fee to do a taker sell in order to get out. This means that nobody who is rational will be offering you the ability to get out and profit from missing the payment that a long holder has to have. Similarly for those who want to make a quick short interest payout, they can't simply short at a market price that will be above spot, allowing them to earn the interest without any cost.

The closer to this 12:00 UTC daily payment, the more the market discount will be to reflect this inability for long or short holders to arbitrage and get a free lunch from this.

Example of Future Value of BTCUSD using BitMEX Swap

Following through with the infographic example and the futures example, let's show what the value of BTCUSD looks like in BitMEX's product.

Assuming the same parameters: 0.05% USD rate, 0.01% BTC rate. Going long at XBTUSD at spot $500 and holding for 7 days results in:

$500*(1+(0.0005-0.0001)*7)=$501.4

This value is identical to that which is seen in the theoretical equilibrium price in prior section for 7-day future price of bitcoin.

Assuming the same parameters: 0.05% USD rate, 0.01% BTC rate. Going long at XBTUSD at spot $500 and holding for 7 days results in:

$500*(1+(0.0005-0.0001)*7)=$501.4

This value is identical to that which is seen in the theoretical equilibrium price in prior section for 7-day future price of bitcoin.

Trading XBTUSD Perpetual Swap in Practice

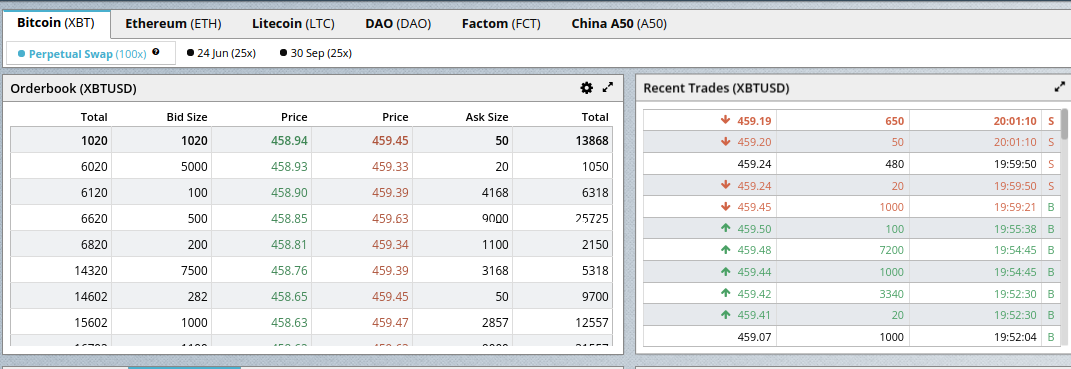

Here's what the orderbook looks like trading XBTUSD. It will be identical to what you're used to if you've traded at BitMEX futures contracts, you have the number of contracts, the price, and it's that simple, long and it goes up makes you profit, short and it goes down and you make profit.

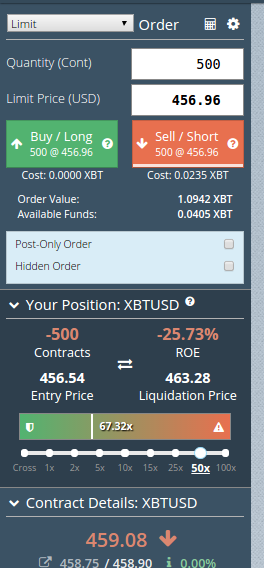

| Just like on the old XBTUSD24H daily contracts, you can go 100x leverage. Meaning you only need 1% margin to trade a position. So if you want to go long with 0.1 BTC then you can take a position as large as 10 BTC! However, this makes you vulnerable to a margin call if the price ends up moving against you in a short time. You can also choose lower leverage, or even Cross Margin if you'd like to use your whole bitcoin balance on BitMEX to cover your positions in a contract. However, it's best to isolate it at some leverage amount, so slide the little slider to indicate how much margin you would like to allocate toward the position. No matter what amount you choose, the XBTUSD swap product has a 0.5% maintenance margin, meaning that when the position goes against you until you only have 0.5% of the notional amount remaining allocated, you will be liquidated. And just like before on BitMEX: the flip side of 100x leverage means that there's socialised losses (called DPE on BitMEX) which can reduce your profits every Friday in the settlement of profit |

This means that when you are trading between Friday evening and next Friday morning, your profits in trading XBTUSD will not be able to be withdrawn until the PNL is settled and any DPE is restarted. This is a minor disadvantage to being able to trade with 100x leverage on a product which essentially tracks spot.

Futures vs. BitMEX Perpetual Swap

The new XBTUSD swap product from BitMEX is a unique and innovative way for traders to speculate on the future value of bitcoin. It has benefits above futures contracts in that they do not expire. When the net financing rate difference between USD and BTC is positive, short holders will earn a daily interest rate payout. If the net financing rate is negative (which is not likely to happen) then long holders would earn daily interest.

One potential downside to this is that while the leverage you access is interest-free, if you're a longholder you will pay financing charges in order to compensate the shortholders for the financing differential in the synthesis explained earlier in this article. However, this is in effect the same as if you were going long on a futures contract at a premium, the difference is that the interest in the swap you pay over time, while the interest in the future is baked into the price.

Don't be scared of the BitMEX XBTUSD swaps. They are really just futures by a different name: you use them in order to speculate on changes in price and you can even earn interest while trading too!

Sign up for BitMEX and get started trading now, get 10% discount on fees.

One potential downside to this is that while the leverage you access is interest-free, if you're a longholder you will pay financing charges in order to compensate the shortholders for the financing differential in the synthesis explained earlier in this article. However, this is in effect the same as if you were going long on a futures contract at a premium, the difference is that the interest in the swap you pay over time, while the interest in the future is baked into the price.

Don't be scared of the BitMEX XBTUSD swaps. They are really just futures by a different name: you use them in order to speculate on changes in price and you can even earn interest while trading too!

Sign up for BitMEX and get started trading now, get 10% discount on fees.

RSS Feed

RSS Feed